Foundations of the Modern World - Interest Rates, Unemployment, and Inflation

Lab Description

This lab consists of two main elements:

- “Building Knowledge” activities where students learn the fundamental concepts of how Interest Rates affect Economic Activity, Unemployment, and Inflation.

- A first-person simulation called “Beat the Fed” where students use their knowledge to manage a modern economy.

Both of these elements provide a high degree of student interaction and opportunities for classroom demonstrations and discussions.

The building knowledge activities are presented using a narrative where the students have been sent back in time and must help the leaders of ancient Sumer use Interest Rates to stabilize their Bronze Age economy. This results in economic concepts that are directly analogous to their modern equivalents but are much simpler to explain and demonstrate. The simplification is the result of the Bronze Age Economy not having the subsequent 5000 years of the invention (trade, fiat money, stock markets, credit instruments, etc) that may cause unnecessary complexity if concepts are introduced in the modern economy.

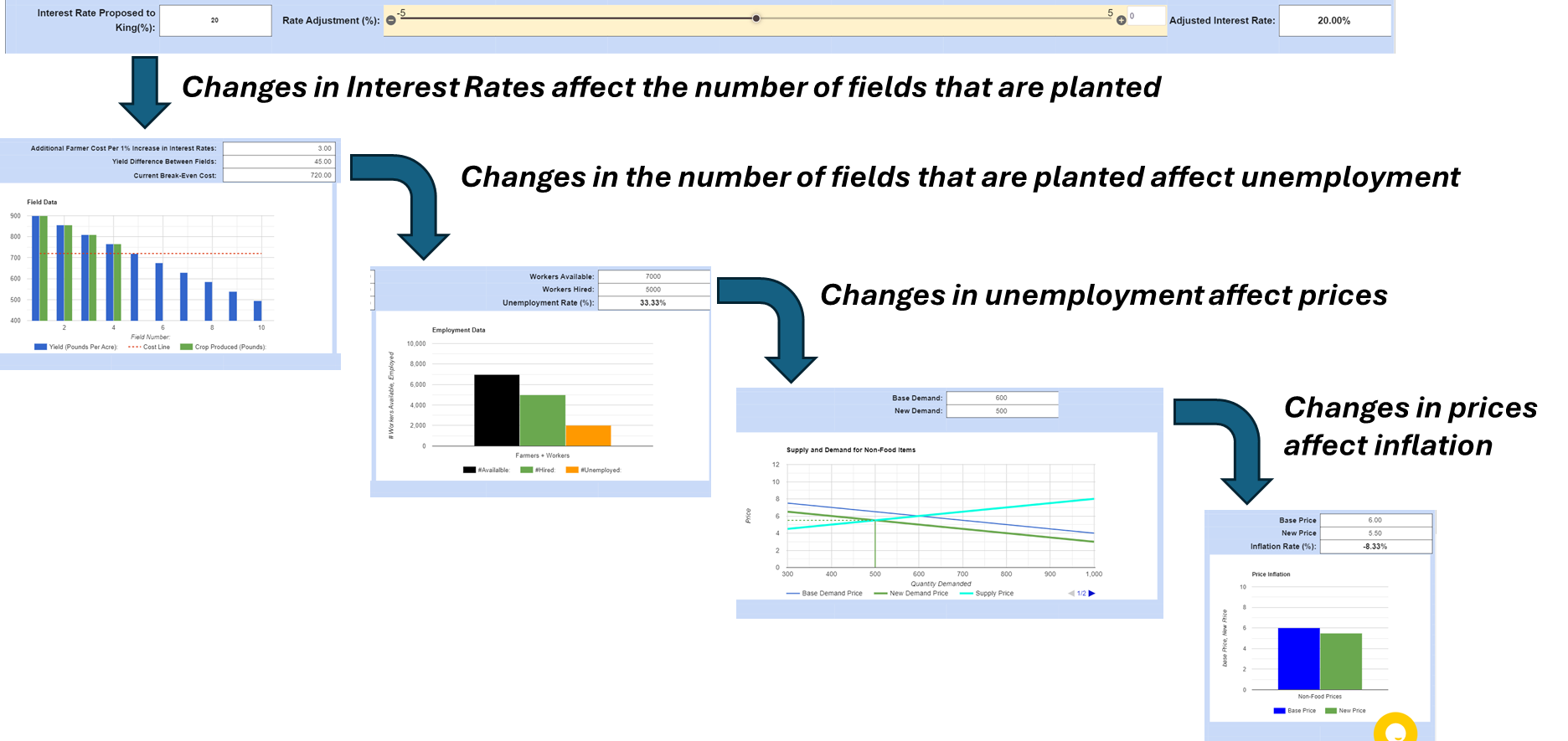

Students learn a series of cause-effect relationships starting with Interest Rates affecting the Number of Fields Planted by Farmers which then leads to effects on Unemployment and Inflation Rates as shown below:

The lab can be run in two days with students being expected to complete a small amount of work outside of class or three days with less outside work and the inclusion of several bonus activities. It is critical that students learn the basic relationships shown on the previous page during the Building Knowledge phase so that these concepts can be reinforced during the Beat the Fed simulation. The ActiveLearningLabs Teacher Console provides real-time reporting of activity completion and score for all students. Since the Building Knowledge Phase includes nearly a dozen activities, you should have a clear picture of student mastery of the content and their readiness for the simulation.